Part 6 of 6 of The Policy-Driven PMA Pivot Series:

While this series has examined the impact of individual policy changes, assessing them in isolation provides only a partial view. In practice, manufacturers will contend with the compounded effect of these policies, as their interdependencies and reinforcing dynamics collectively redefine the pricing and access landscape. The combined effects of the IRA, MFN, FTC actions, PBM reform, and related policies are expected to drive several structural shifts. Most notably, they may contribute to a bifurcation in pricing models – accelerating a transition toward “lower-list, lower-rebate” frameworks for some product archetypes, while reinforcing the persistence of “high-list + rebate” models for others. This dynamic is explored further through two illustrative analogues later in this paper: GLP-1s in cardiovascular-renal-metabolic conditions, and CD20-directed therapies in autoimmune CNS disease. Beyond pricing, these intersecting policies introduce a set of multiplicative pressures, including heightened constraints on manufacturer economics and value expectations, as well as an imperative to evolve channel and access strategies.

With respect to constraints on manufacturers, the IRA-driven redesign of the Part D benefit has materially increased plan liability, contributing to an exodus of payers from the Part D market. This shift is likely to introduce new affordability challenges for patients, as product-specific access becomes more fragmented and less predictable for Medicare beneficiaries. At the same time, the effect of increased financial exposure from the IRA is compounded by MFN-driven price transparency and further heightens payer sensitivity to higher prices. Together, these dynamics raise the bar for manufacturers to demonstrate value through more rigorous clinical evidence, clearer differentiation, more robust real-world evidence strategies, and, in some cases, innovative portfolio-based contracting approaches, particularly in competitive markets with low-cost generics or entrenched brands. In effect, manufacturers will need to be prepared to operate with reduced pricing flexibility and rising evidence expectations, necessitating tighter coordination between access and medical/HEOR functions, along with more dynamic and continuous price sensitivity assessment as the landscape continues to evolve.

Concurrently, disruption of the traditional PBM model for certain product archetypes is driving margin compression and prompting a fundamental reset of pricing and access strategies. As PBM reform intersects with the rise of HDHPs/HSAs1 and increased momentum toward direct-to-consumer distribution spurred by MFN transparency and emerging direct distribution models (e.g., Cost-Plus, TrumpRx), new stakeholders, including patients and employers, are taking on a more prominent role in decision-making. In this evolving landscape, manufacturers will need to shift from a primary focus on PBMs and rebate optimization toward a more holistic channel strategy, including investment in direct-to-consumer and direct-to-employer capabilities, reimagined patient support and hub models, and a more deliberate evaluation of which products may benefit from direct distribution as a margin defense strategy.

Ultimately, navigating this increasingly complex policy environment will require a product- and archetype-specific approach, as well as a partners capable of helping patients navigate alternative channels. Key considerations, including benefit design, channel and book-of-business mix, therapeutic areas and indications of focus, and competitive intensity, will inform the most effective path forward for pharmaceutical manufacturers. The following sections begin to outline archetype-based strategic imperatives in more detail, reflecting the types of strategic questions and analyses Triangle addresses in close partnership with clients.

Compounding Policy Effects on Price and Access: Archetype Case Studies

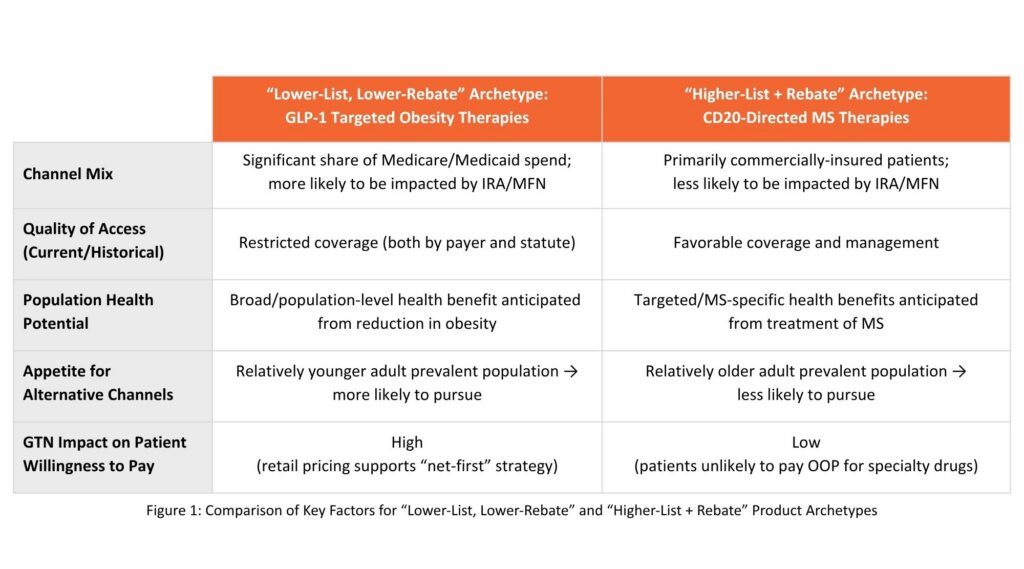

To emphasize the interplay of these policies and understand the impact on pricing and access strategy, consider two product archetypes: a product appropriate for a “lower-list, lower-rebate” (“net first”) strategy vs a more traditional “higher-list + rebate” strategy.

Example characteristics of a product that may be more likely to implement a “lower-list, lower-rebate” pricing strategy include products with

- Significant potential market share in government channels (particularly Medicare/Medicaid)

- Access restrictions that may encourage distribution through alternative access models

- A large patient population with appetite for purchasing through alternative channels (particularly for “lifestyle,” acute/on-demand, or retail-priced products for younger adults)

- A GTN that limits patient willingness to pay.

These factors (outlined in Figure 1) and their aggregate impact can be seen in the evolution of the pricing model for GLP-1 therapies, such as semaglutide (Wegovy, Ozempic, Rybelsus) and tirzepatide (Zepbound, Mounjaro). Upon expansion from type 2 diabetes into obesity, coverage became extremely restricted under many plans and channels to control costs as patient demand surged, with an untapped market in Medicare due to statutory exclusion of obesity medications. GLP-1 drugs were thus primed for distribution through alternative models to initially optimize patient access, and to later on limit the potential impact of restrictions in Medicare/Medicaid. Alternative models (e.g., direct-to-patient, direct-to-employer) will also continue to encourage lower list prices for a “lifestyle” medication with population-level demand and potential health benefits (e.g., secondary to significant weight-loss). At the same time, policies such as MFN and IRA dovetail with “lower-list, lower-rebate” pricing and direct-to-stakeholder approaches for GLP-1s. MFN GENEROUS may expand access to GLP-1s in Medicaid (lower prices may come with reduced utilization management for participating state Medicaid plans, and their MCO-managed counterparts in those states, as part of GENEROUS model negotiations). Medicare price negotiations under IRA underscore the value of GLP-1s to the channel as well as a price benchmark for other payer channels, reducing patient OOP costs as a result in a patient population that historically has shown less appetite to pursue alternative channels. Altogether, GLP-1 drugs represent a clear example of a class evolving to a “lower-list, lower-rebate” strategy across the five example characteristics in Figure 1.

In contrast, key features of a product archetype more likely to retain traditional “higher-list+ rebate” pricing include:

- A primarily commercially insured patient population with favorable access,

- A more indication-specific than population-level addressable market with less appetite to purchase through alternative channels (particularly for chronic, disease-specific, and specialty-priced products for older adults)

- A GTN that doesn’t materially impact patient willingness to pay.

These factors (outlined in Figure 1) are hypothesized through CD20-directed cytolytic antibodies for the treatment of multiple sclerosis (MS). Approximately 75% of MS patients are commercially insured3, translating to minimal spend from the Medicare/Medicaid channels (and thus a more limited impact of IRA/MFN on pricing decision-making). CD20-directed antibody therapies have shown strong clinical differentiation and value with significantly reduced relapse rates compared to other MS treatment classes4 (e.g., pyrimidine synthesis inhibitors), resulting in favorable payer access. While MS represents a significant healthcare burden unto itself, its treatment does not bring the population-level cross-indication benefits of GLP-1 therapy. Further, channeling MS treatments through alternative distribution models would be more dependent upon patients north of middle age that may be less primed to pursue such models than younger patients. Lastly, the pricing dynamic of MS therapies vs GLP-1 therapies (specialty vs retail) remains important to consider – movement to a “net first” pricing strategy for MS brands would do little to increase patient willingness to pay in either traditional or alternative channels. Altogether, these factors support maintenance of traditional “higher-list + rebate” pricing strategies, with CD20-directed antibody therapies for MS offering a hypothesized archetype to contrast with GLP-1 therapies.

Strategic Considerations

As manufacturers launch new therapies into an ever-evolving pricing and access landscape, Triangle Insights encourages manufacturers to consider the following when evaluating potential pricing and access strategy:

- What share of Medicare/Medicaid spend is allocated to this indication and class of drugs? To what extent is the patient population insured through commercial versus public channels?

- To what extent have competitor drugs been targeted by (or responded to) major drug pricing policy reforms such as IRA and MFN?

- What evidence may payers require to support favorable access as payers face greater cost exposure and liability from policy changes?

- What volume benefit might be gained through use of alternative rather than traditional access models? Do the population and drivers to pursue alternative channels align with your product?

- Does a reduced GTN materially affect the patient value proposition / willingness to pursue and pay for your therapy (e.g., opening up access for new demographics or use cases)?

While GLP-1 and CD20 targeted therapies represent contrasting examples across the factors outlined in Figure 1, and the questions highlighted above, it is anticipated that most manufacturers considering a “net first” pricing strategy will encounter products that share a mix of factors.

This concludes our 6 part series, check out Part 1 to explore the full picture.

References

- Kaiser Family Foundation. “Policy Changes Bring Renewed Focus on High-Deductible Health Plans.” Accessed March 2026.

- IBM Micromedex RED BOOK. IBM Watson Health; 2026. Accessed April 2026.

- Miller, D, et al. “Assessing Access to Five Types of Insurance by People with Multiple Sclerosis Using a Cross-sectional Online Survey.” International Journal of MS Care, vol. 23, no. 6, 2021, pp. 253–260. DOI: 10.7224/1537-2073.2020-062.

- Novartis Pharmaceuticals Corporation. Clinical trial results | KESIMPTA® (ofatumumab). Accessed April 10, 2026.